The Tariff Tightrope: How May’s CPI Dip Masks Mortgage Rate Risks

May’s CPI eased to 2.4%, but tariffs & Fed policy threaten 7% mortgage rates. Discover how inflation divides homeowners & buyers in 2025.

May’s CPI Report: A Sigh of Relief?

The May Consumer Price Index (CPI) surprised economists, rising just 0.1% month-over-month and 2.4% annually—slightly below forecasts. Core CPI (excluding food and energy) also cooled to 2.8% yearly, hinting at easing inflation. Gasoline prices fell 2.6%, while airfares, smartphones, and used cars dropped sharply. But don’t celebrate yet: bananas, peanut butter, and appliances spiked 3% or more, proving pain persists for household budgets.

Why This Calm Won’t Last

Federal Reserve Governor Christopher Waller warns today’s mild data is a “reassuring but fragile” pause. Trump’s tariffs—slapped on $300B+ of imports—have barely hit consumer prices. The average effective tariff rate surged from 2% to 14% in a year, yet the full impact is delayed like a “slow-motion tsunami”. UBS predicts core CPI could leap to 3.9% by late 2025—a level unseen since the 2022 inflation crisis.

Mortgage rates hit 7% in 2025 as Fed battles inflation | FLASH FACTZ

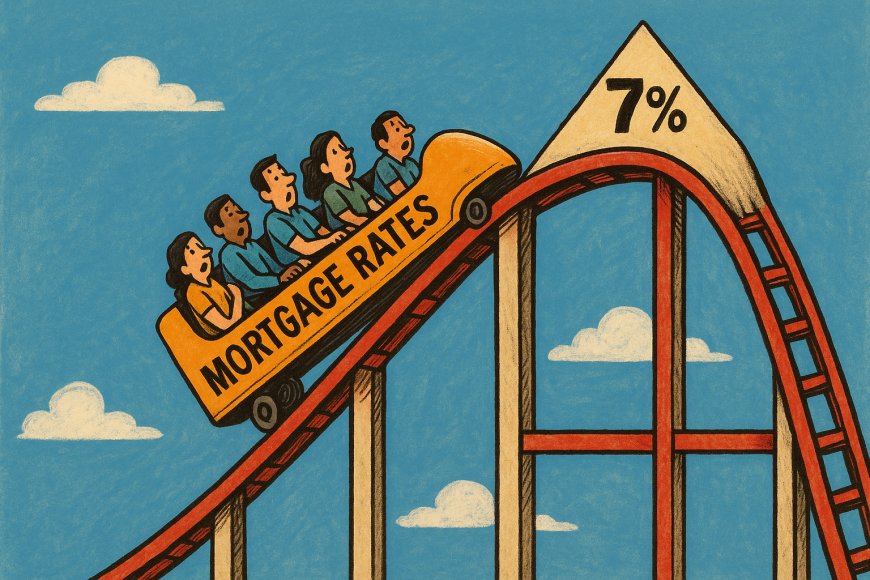

Mortgage Rates: Stuck at 7%? The Fed’s High-Wire Act

The Fed’s Inflation Fight

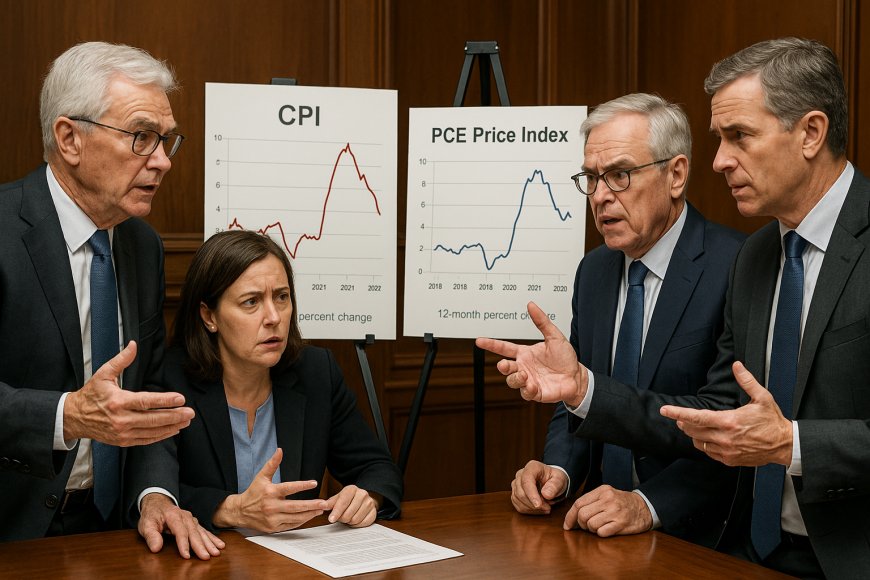

Mortgage rates aren’t set by inflation alone—but the Federal Reserve’s response to it is pivotal. Here’s the domino effect:

- CPI and PCE reports guide Fed policy.

- To cool inflation, the Fed hikes the federal funds rate (banks’ overnight lending rate).

- Banks then raise consumer loan rates, including mortgages, to protect profits.

After May’s CPI, traders see near-zero chance of a June rate cut. FedWatch data shows markets betting rates hold at 4.25%-4.5% until at least July. Translation: mortgage rates won’t dive soon.

Current Mortgage Landscape

- 30-year conforming loans: 7% (up from 6.69% in April).

- FHA loans: 6.68%, marginally lower.

- Jumbo loans: 6.79%, stable but steep.

The Fed’s 2% inflation target remains elusive, and until it’s within reach, rate cuts are off the table.

Trump tariffs could triple iPhone prices warns economist Scott Galloway | FLASH FACTZ

Tariff Tinderbox: How Trump’s Trade War Could Ignite Inflation

Scott Galloway’s “Blackout Drunk” Warning

NYU professor Scott Galloway unleashed fiery criticism of Trump’s tariffs, calling them economically “stupid” and akin to having someone “blackout drunk at the wheel” of the global economy. His logic:

- Tariffs on Chinese goods could triple iPhone prices (e.g., from $1,000 to $3,500).

- Outsourcing low-wage jobs lets the U.S. focus on high-value innovation—a advantage now at risk.

JPMorgan echoes this, warning “meaningfully larger [price] increases are likely in coming months”. Even a 90-day U.S.-China tariff truce in May offers only fleeting relief.

Housing’s Hidden Tariff Time Bomb

Building materials (steel, lumber) and labor costs could surge as tariffs trickle through supply chains. Result? Higher home prices and closing costs (appraisals, inspections). Pulte Homes’ CEO warns if tariffs inflate rates further, the housing market’s “tepid recovery” could stall.

Federal Reserve debates rate cuts after May CPI data misses targets | FLASH FACTZ

Homeowners vs. Buyers: Inflation’s Uneven Playground

Winners: Existing Homeowners

Inflation boosts home equity as property values rise. Sellers could pocket bigger profits—if they time their exit before higher mortgage rates dent demand.

Losers: Buyers

They face a double whammy:

- Mortgage rates near 7% (vs. 3% in 2021).

- Home prices inflated by tariff-driven construction costs.

The silver lining? Reduced competition as others get priced out.

Home buyers face double squeeze from inflation and mortgage rates in 2025 | FLASH FACTZ

The GSE Wildcard: Could Fannie and Freddie’s “Release” Roil Rates?

Trump’s plan to privatize Fannie Mae and Freddie Mac—in conservatorship since 2008—could backfire. Industry leaders fear:

- Removing government backing might force lenders to hike rates to offset risk.

- UWM CEO Mat Ishbia warns: “If interest rates go up because of this change, I don’t think they’re going to do it”.

A Bloomberg report suggests a compromise: a public offering with federal oversight to avoid market chaos.

Homeowners gain equity as buyers struggle with inflation in 2025 | FLASH FACTZ

Future Forecast: Will 2025 Bring Relief?

The Crystal Ball Says... Maybe

- Fannie Mae projects 30-year rates falling to 6.1% by December.

- Fed inflation forecasts sit at 3.2% for 2025—still too high for swift rate cuts.

But curveballs lurk:

- Tariff impacts hitting CPI in Q3/Q4.

- Job market heat (unemployment at 3.9%) giving the Fed pause.

- Data reliability issues as the Bureau of Labor Statistics cuts survey samples due to a federal hiring freeze.

Fact 1: May’s mild CPI is a calm before the storm. Tariffs could spike inflation by late 2025, torpedoing rate-cut hopes.

Fact 2: 7% mortgages are the new normal—blame the Fed’s inflation fight and GSE uncertainty.

Fact 3: Homeowners gain equity wealth in inflation surges; buyers pay the price in rates + home costs.

What's Your Reaction?